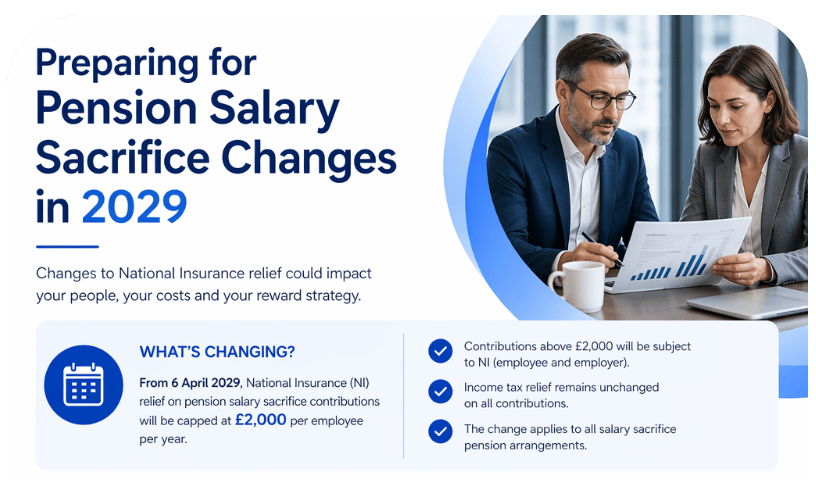

What’s changing?

The government has announced that from 6 April 2029, National Insurance (NI) relief on pension salary sacrifice contributions will be capped at £2,000 per employee per year.

Under the new rules, only the first £2,000 of employee pension contributions made through salary sacrifice in each tax year will be exempt from employee and employer NI contributions. Any pension contributions sacrificed above £2,000 will be liable for NI, although pension contributions will continue to benefit from Income Tax relief, subject to normal pension tax limits.

What does this mean for employees?

For many workers who contribute less than £2,000 a year (£166.66 per month) via salary sacrifice, there will be little or no change. However, employees making larger pension contributions may see reduced National Insurance savings from April 2029. Higher earners are expected to be the most affected by the reform.

What does this mean for employers?

Employers can continue offering salary sacrifice pension schemes, but payroll systems will need to calculate National Insurance on any salary sacrifice above the annual £2,000 threshold. Organisations with generous pension schemes may also need to review their reward strategies and communicate the changes well in advance of implementation.

Preparing for 2029

Although the changes do not take effect until April 2029, employers should use the transition period to assess the impact on payroll, budgeting and employee communications. Reviewing existing salary sacrifice arrangements now can help ensure a smooth implementation when the new rules come into force.